In 1C 8.3 there are several documents that relate to the commission trading section. One of them is the “Report of the commission agent (agent) on sales.” This document is drawn up according to the information of the agent to whom our organization has instructed to sell its goods.

The document “Report of the commission agent (agent) on sales” works in conjunction with other documents, so it is worth considering the entire chain:

- Transfer of goods to the agent;

- Sales agent report;

- Receipt of funds from the agent;

- Return of unsold goods.

The connecting link for all of the above operations is the contract. Let's consider the features of its design (Fig. 1).

The basic rule when drawing up an agency agreement is to indicate the desired type, namely “With a commission agent (agent) for sale.” The type of agreement will subsequently determine the behavior of all documents in our chain.

The price type and commission calculation method are not required to be filled in, but it is advisable to avoid unnecessary manual calculations.

Transfer of goods for commission

The first document is “ ” (Fig. 2). The same document is used to reflect any sales operations, but in our case an invoice is not issued for it.

The same document is used to reflect other sales transactions, but unlike them, in our case, an invoice is not issued for it, and when carried out there is no VAT posting (Fig. 3). This “behavior” is determined by the type of contract.

Since finished products are transferred to the commission, the amount of the transaction is equal to the previously calculated cost.

Agent's report on the goods sold

Finally, you can create an agent report in 1C 8.3. It can be filled out based on the implementation document (Fig. 4). The document is multi-page, let's look at it in more detail.

Get 267 video lessons on 1C for free:

On the main page we check the settlement accounts. We make payments for goods using account 76.09; for remuneration – 60.01, 60.02; Remuneration costs are charged to account 44.01.

On the same page we register an invoice for the agent’s remuneration.

On the second page (“Sales”) the data of the final buyer and the list of goods sold are indicated (Fig. 5).

If the buyer was , the corresponding flag is set and the invoice date is indicated. After posting the document, an invoice will be generated automatically (Fig. 6).

The third page records the amounts of money received from the buyer for the goods (Fig. 7).

Unsold goods can be indicated on the “Returns” page.

Receipt of reward to the current account

Based on the agent’s report in 1C 8.3, you can generate a cash flow (Fig. 9). The agent is obliged to transfer the amount received from the sale of commission goods minus his remuneration.

Checking amounts for account 76 and sales book

Mutual settlements are checked using the balance sheet for account 76.09 (Fig. 10). In our case, the remainder is zero; goods were sold for the amount of 2,000 rubles, of which 200 rubles. the agent received as a commission (this is 10% of the sale amount, as specified in the contract), and 1,800 rubles. listed to the seller by the agent.

Finally, let's check the sales book. It should contain a record of the sale of goods through an intermediary (Fig. 11). As you can see, the required record exists, and both the final buyer and the intermediary are indicated in it, i.e. our agent. This data is taken from the invoice issued in the document "

Almost all companies on the market now provide certain services to their clients. They can be one-time or monthly, mass or individual.

The 1C accounting program we are considering provides various ways of registering and accounting for the provision of services, for example, through “Sales (acts, invoices).” Let us give examples of the use of different methods of reflecting the provision of services.

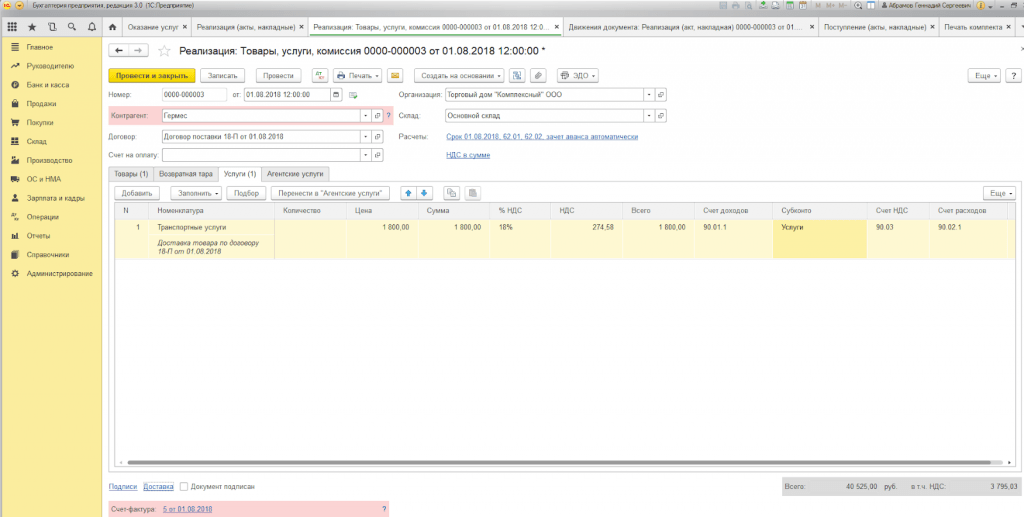

Example 1. LLC "Trading House "Complex" entered into an agreement for the supply of goods. Delivery is carried out by the company at the expense of the buyer.

For registration, we use the document “Sales (acts, invoices)”, which can be accessed through the “Main Menu – Sales”.

If it is necessary to issue a single invoice for the supply of goods with delivery, we use the “Goods, services, commission” option, which we find in the “Create” submenu.

Fill out the “Product” and “Services” tabs.

When choosing to print a set of documents, you can specify the number of copies of those forms that are used in your company's document flow.

The printed form of the act of provision of services in the 1C program is standardized, but can be developed by the company independently.

Example 2. An agency agreement was concluded between Primer USN-15 LLC and FORK LLC for services for the collection and preparation of documents for obtaining a security license on its own behalf. This provides for a remuneration for the agent - 10% of the price of services provided, which is calculated from the received DS from buyers.

To display settlements with the buyer with the participation of an agent, the document is drawn up in the same way as in Example 1, but we also fill in “Agency services”.

The settlement account is located automatically, and postings are generated when posting the document.

Upon completion of the services, our company must give the principal a report on the transactions. To do this, and to display the commission, we will create a “Report to the Principal”.

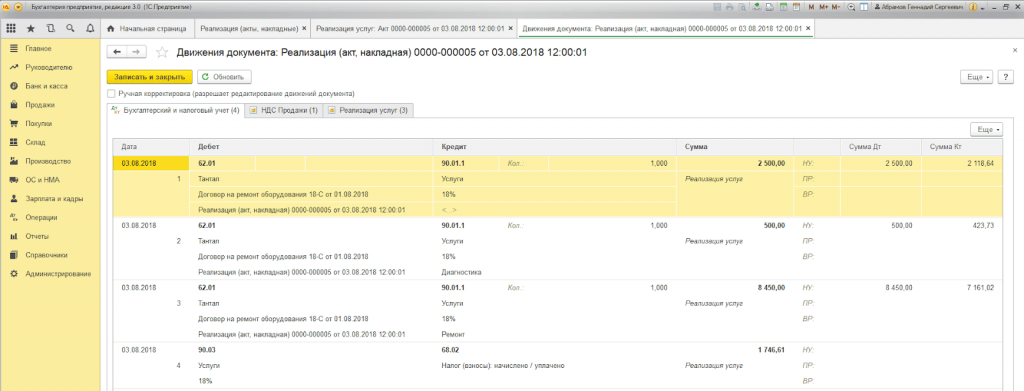

Example 3. LLC "Trading House "Complex" provides service center services for equipment repair.

If we need to reflect the performance of a one-time service or a list of works for an individual order of the buyer without shipping goods, we can use the “Services (Act)” transaction type. We look for the type of operation required in the “Create” submenu.

The tabular part indicates the list of works, and if the service is one-time in nature, you can, without filling out the “Nomenclature” directory, enter a description of the work performed manually.

When posting a document, postings are generated.

A distinctive feature in 1C:Enterprise 8.3 is the presence of the “Provision of Services” document, with the help of which services of a mass nature with a specified frequency are quickly and accurately executed. These services include:

- Service cards in fitness centers (annually);

- Subscriber service for accounting (quarterly);

- Rent in business and shopping centers (monthly);

- IT infrastructure maintenance services (monthly);

- Communication services (monthly), etc.

Thus, the provision of services in 1C 8.3 can be carried out with one document to an unlimited number of clients whose agreement is tied to a specific type of payment.

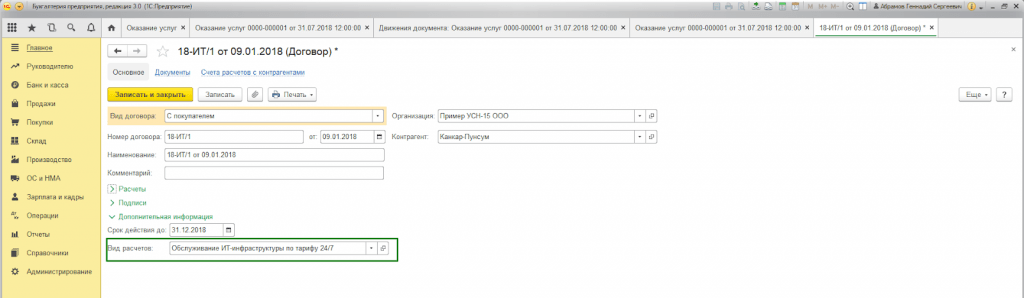

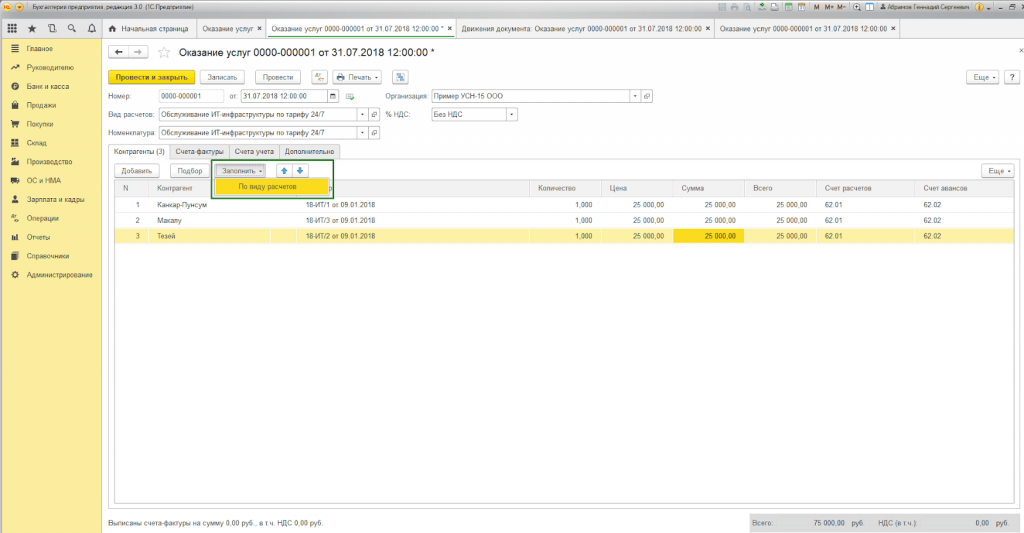

Example 4. Primer USN-15 LLC provides IT infrastructure maintenance services. Subscriber service agreements have been concluded with a number of clients at a 24/7 tariff costing RUB 25,000/month.

First of all, you need to check the possibility of batch issuing acts and invoices in the program functionality settings on the “Trade” tab (Main - Settings - Functionality).

Also, when drawing up an agreement with the buyer, it is necessary to fill in the “Type of settlements”* in the “Additional information” block.

*Type of calculations – reference book (text line), which is filled in by program users independently, depending on the required grouping of buyer contracts.

To formalize the mass provision of services, we use the “Provision of Services” document, which can be accessed through the “Main Menu – Sales”.

In the document header, you must select from reference books of the same name:

- Nomenclature.

The “Nomenclature” field is necessary to fill in the name of services in the work completion certificate. Moreover, if the “Frequency of service” attribute is set in the “Nomenclature” directory, then the printed form of the act will automatically set the period for which the document is generated.

Thus, there is no need to enter several elements of the “Nomenclature” directory for different periods (rent May 2018, rent June 2018, etc.) or manually adjust the printed form.

The “Fill in by calculation type” button automatically fills in the tabular part of the document.

The “Counterparties” tab (list) displays all buyers whose contract contains the “Type of settlement” attribute specified in the header of the document.

On the “Invoices” tab, the list indicates clients to whom, under the terms of the contract, we provide an invoice for work performed, regardless of the taxation system used by our organization. When posting, the “Invoice issued” document is generated automatically.

Document movements reflect accounting and tax accounting entries, as well as filling out the accumulation register “Sales of services”.

A printed form of the document is generated for each buyer reflected in the document. Numbering is set automatically.

Accounting for the provision of services in 1C 8.3 using any method of registration will lead to the correct generation of accounting and tax reporting. The choice of document form is not regulated, but is chosen by the user based on the convenience of filling out and processing documents.

We made a document for the sale of services with the type of operation - Intermediary service - when posting the document we received the following postings:

- D76.5 client

- K 76.5 Transcontainer -1000.00

VAT was not allocated separately and the amounts went entirely to 76. Based on this document, an invoice was issued, but it was not entered into the database so that it would not end up in the sales book.

Then, using an accounting certificate, they transferred these amounts to their parent company:

- D76.5 Transcontainer

- K 79.2 Parent organization -1000.00

In 1C Accounting 8.3 we also create a document for the sale of agency services, but it breaks down the amount for us and is reflected in 90.01.1, 90.3, 68.2.

How can we configure the service sales document so that there is one posting:

- D76.5

- K 76.5

with VAT reflected in the document.

Answer Profbukh8

Elena Bobkova (Master group website)

Good evening!

To sell services under an agency agreement in 1C 8.3 to the customer, use the document “Sales of goods and services” with the view “Goods, services, commission”.

For the scheme to work correctly, it is necessary to select the type of contract with the principal as “ ”, and with customers of services - “With the buyer”.

- In the “Implementation of technical and technical management” document, select the customer as the counterparty and indicate the contract with him. Using the “Settlements” hyperlink, you can set up the account you need for settlements with the customer. The developers recommend 62. You can set up VAT accounting here.

- Fill out the “Agent Services” tab. Here, in the services line, indicate the principal in the “Counterparty” column and in the Agreement column - the agency agreement with him. Next, the accounting account that you use to pay the principal. The developers have 76.09 in their recommendations.

Write down the document and look at the postings: (I am writing according to the recommendations of the developers) Dt 62/Kt76.

From this document you can immediately create an invoice for the customer. Don’t forget to “track” the transaction code - 04. S/f will not provide postings, but will create the necessary entry in the Invoice Journal.

For mutual settlements with the principal, it is created. But here you need to look at everything directly on your base and contracts.

I gave you a schematic diagram in 1C 8.3. Good luck)

Please rate this question:

(1 ratings, average: 5,00 out of 5)

In trading activities, enterprises use the services of intermediaries. Intermediary operations must be formalized by appropriate agreements, which are divided into: agency agreement, commission agreement and agency agreement.

In accordance with Ch. 52 of the Civil Code of the Russian Federation, under an agency agreement, one party (agent) undertakes, for a fee, to perform, on behalf of the other party, the principal (principal), legal and other actions on its own behalf, but at the expense of the principal, or on behalf and at the expense of the principal.

Let's look at an example. The organization (Agent) entered into an agency agreement with the principal to provide services on its own behalf. The agency fee is 5% of the cost of services sold and is deducted from funds transferred by buyers.

To be able to reflect agency transactions in the 1C: Accounting 8 edition 3.0 program, you need to configure the program. Why check the necessary items in the Program Functionality on the Trade tab? In our case, this is the sale of goods or services of the principals (principals) (Fig. 1).

To implement the above example in the program, we will need the following documents:

- Sales (Act, invoice)

- Report to the committent

In the Sales section, we will create a document Sales (Act, invoice) with the transaction type Goods, services, commission. In the header of the document, fill in the details of the Counterparty and the contract - the type of contract with the buyer. In the tabular part on the Agent services tab we will indicate the nomenclature - the service, its cost, VAT rate. In the counterparty and agreement field, we indicate the principal and the agency agreement (the type of agreement must be With the principal (principal) for sale). The contract can specify the option for calculating the agency fee. The settlement account is automatically set to 76.09 “Settlements with various debtors and creditors”. Let's review the document. We will issue an invoice (Fig. 2).

If the agent sells goods (work, services) of the principal on his own behalf, then the invoice is issued by the intermediary in duplicate on his own behalf. One copy of this document is handed over to the buyer, and the second is filed in the journal of issued invoices without registering it in the sales book.

After the sale of services, the agent must submit a transaction report to the principal. To perform this operation, as well as to reflect the commission, we need to create a Report to the Principal document, which is located in the Purchases section. On the Home tab, select the principal and the agency agreement. The method for calculating the commission will be entered automatically, since we initially specified it in the contract. It is necessary to create the Remuneration service; accounting accounts will be automatically filled in based on the “Item Accounting Accounts” register. On the Goods and Services tab, fill out the tabular section by clicking the Fill button - Fill in sold under the contract. We will issue an invoice for the remuneration and look at the document entries. We see that our revenue has been reflected and VAT has been charged. The document settings are shown in Fig. 3.

Upon receipt of the agent's report, the principal must issue invoices for each buyer. The Agent must receive copies of invoices and record them in the Invoices Received and Issued Log by date of receipt.

Invoices received from the principal are created based on the report to the principal. In the Invoice received document, you must indicate the number and date, and in the Invoice issued to buyers field, select the invoice issued by the agent to the buyer upon sale (Fig. 4).

Now we need to generate reports and make sure that our actions are correct. In the Reports section, we will create a Journal of received and issued invoices (Fig. 5) and a sales book (Fig. 6).

Company GARANT

The organizations concluded. Both the principal and the agent apply the same taxation system. In accordance with the concluded agreement, the agent, on its own behalf, enters into contracts with customers for the transportation of goods by the principal. The terms of the agency agreement assume that all rights and obligations under contracts concluded with customers arise with the agent. The agent makes settlements with the principal after the receipt of funds from the customer to the agent, withholding the remuneration due to him.

What is the procedure for document flow between the parties in this situation? What is the procedure for accounting and tax accounting of cash receipts from customers for the principal and the agent?

Chapter 52 of the Civil Code of the Russian Federation (hereinafter referred to as the Civil Code of the Russian Federation) regulates the relationship between the parties under an agency agreement. In addition, the rules of the Civil Code of the Russian Federation on commission agreements (Article 1011 of the Civil Code of the Russian Federation) apply to an agreement under the terms of which the Agent acts on his own behalf (and in the situation under consideration, the Agent acts on his own behalf).

Under an agency agreement, one party (Agent) undertakes, for a fee, to perform legal and other actions on behalf of the other party (Principal) on its own behalf, but at the expense of the Principal or on behalf and at the expense of the Principal. At the same time, under a transaction made by the Agent with a third party on his own behalf at the expense of the Principal, the Agent acquires rights and becomes obligated, even if the Principal was named in the transaction or entered into direct relations with the third party for the execution of the transaction (Article 1005 of the Civil Code of the Russian Federation) .

Everything received by the Agent under the agency agreement is the property of the Principal (Article 974 and clause 1 of Article 996 of the Civil Code of the Russian Federation, Article 1011 of the Civil Code of the Russian Federation, see also letters of the Federal Tax Service of Russia dated 02/28/2006 N MM-6-03/202@, dated 04.02 .2010 N ShS-22-3/85@, letter of the Ministry of Finance of Russia dated 10/02/2009 N 03-07-11/246).

The agent receives remuneration for services rendered, the amount and payment procedure for which are established by the agency agreement (Article 1006 of the Civil Code of the Russian Federation). At the same time, Article 997 of the Civil Code of the Russian Federation gives the commission agent the right (as stated above, if the Agent acts on his own behalf, then the rules on the commission agreement are applied) in the order of offsetting counter homogeneous claims (Article 410 of the Civil Code of the Russian Federation) to withhold the amounts due to him under the commission agreement from all amounts received by him at the expense of the principal.

As can be seen from these norms, civil law gives the Agent the right to withhold the remuneration due to him from amounts received from third parties in pursuance of an agreement concluded by the Agent on behalf of the Principal. In this case, the parties have the right to agree in the agency agreement, at their discretion, on the conditions and procedure for paying remuneration to the Agent (clause 2, article 1, clause 4, article 421 of the Civil Code of the Russian Federation).

Document flow

The Agent is obliged to provide the Principal with reports on his performance of the agency agreement in the manner and within the time limits provided for by the agreement. If there are no specific conditions for the submission of reports in the contract, they are submitted by the Agent as he fulfills the contract or upon expiration of the contract (Article 1008 of the Civil Code of the Russian Federation). In this case, the Agent’s report must be accompanied by the necessary evidence of expenses incurred by the Agent at the expense of the Principal (unless otherwise provided by the agency agreement). Consequently, the question of which documents confirm the execution of the agency order and should be attached to the Agent’s report is decided by the parties at their own discretion (the list of documents is provided for in the agency agreement).

It should be noted that the Agent’s report is the primary accounting document for the Principal, confirming the expenses incurred in the form of agency fees and expenses reimbursed to the Agent (letter of the Federal Tax Service of Russia for Moscow dated April 5, 2005 N 20-12/22797, resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated February 14. 2012 N 12093/11, resolution of the Federal Antimonopoly Service of the North Caucasus District dated 06.06.2012 N F08-2678/12).

In the situation under consideration, the Agent attracts Customers to transport goods by the Principal and enters into contracts with them on its own behalf. In this case, documents on transactions concluded by the Agent with the Customers (invoices, certificates of completion of work (services rendered), invoices, etc.) are issued by the Agent to the Customers on its own behalf. In this connection, we believe that certificates of work performed by the Principal are not issued to Customers (Customers will have certificates of work completed from the Agent). Also, in our opinion, the Principal does not need to duplicate the act issued by the Agent to the Customer (that is, reissue it to the Agent). At the same time, in order to reflect in the Principal’s accounting operations for the implementation of work (services) carried out under the agency agreement, the Principal must have an Agent’s report (agent’s notice) with copies of supporting documents attached. If the agency agreement provides for the drawing up of an act for the agency fee, then the Agent draws up such an act.

The Agent's report and act are drawn up in any form, since no special rules regarding their form and content are established by law. In this connection, in the agency agreement, the parties can independently determine the form of these documents and the list of information required by the Principal. Please note that it is necessary that all specified primary documents (including the agent’s report and act) contain all the mandatory details established by clause 2 of Art. 9 of the Federal Law of December 6, 2011 N 402-FZ “On Accounting”.

Operations for the sale of goods (works, services) on the territory of the Russian Federation are recognized as subject to VAT (clause 1, clause 1, article 146 of the Tax Code of the Russian Federation). At the same time, the implementation of works (services) by the Principal is subject to VAT, regardless of whether the Principal carries out their implementation on its own behalf, or through an intermediary under an agency agreement.

By virtue of clause 3 of Art. 168 of the Tax Code of the Russian Federation, when selling goods (work, services), as well as upon receiving amounts of payment, partial payment on account of upcoming deliveries of goods (performance of work, provision of services), the corresponding invoices are issued no later than five calendar days counting from the day of shipment of the goods (performance works, provision of services) or from the date of receipt of payment amounts, partial payment on account of upcoming deliveries of goods.

An invoice is a document that serves as the basis for the buyer to accept the goods (work, services) presented by the seller (including the commission agent, agent who sells goods (work, services), property rights on their own behalf) for deduction of VAT amounts (clause 1 of Art. 169 of the Tax Code of the Russian Federation).

Thus, the Agent is obliged, no later than five calendar days from the date of sale of services to the buyer (Customer), to issue a corresponding invoice in the name of the buyer (Customer), highlighting the amount of VAT.

The specifics of filling out documents used in calculating value added tax when carrying out intermediary transactions are established in the appendices to Resolution of the Government of the Russian Federation dated December 26, 2011 N 1137 (hereinafter referred to as Resolution N 1137).

Since, according to the agency agreement, the Agent acts on his own behalf, invoices to buyers (Customers) with the allocation of the amount of VAT must be issued by the Agent on his own behalf, and the details of these invoices must be transferred to the Principal (clause 20 of the Rules for maintaining the sales book used in settlements for value added tax of Resolution No. 1137). That is, the Agent, in the invoice issued to the buyer of services, indicates the name of his organization as the seller in accordance with the constituent documents (letter of the Ministry of Finance of Russia dated April 29, 2013 N 03-07-09/15077). Additionally, the Agent can also indicate information about the Principal and the agency agreement (letter of the Ministry of Finance of Russia dated April 23, 2012 N 03-07-09/40).

Invoices issued to buyers (Customers) are registered by the Agent only in part 1 of the log of received and issued invoices used in calculations of value added tax, Resolution N 1137. These invoices are not registered by the agent in the sales book (clause 20 Rules for maintaining a sales book used in calculations of value added tax, Resolution No. 1137).

At the same time, the Agent informs the Principal of the details of the invoice issued to the buyer (Customer).

The Principal, in turn, must issue to the Agent invoices that reflect the indicators of the invoices issued by the Agent to buyers (Customers), as well as invoices upon receipt of the payment amount (partial payment), which reflect the indicators of the invoices, issued by the Agent to buyers (Customers), and register them in the sales book. Therefore, the Principal, based on the data received from the Agent about the services (works) implemented, issues an invoice to the Agent on the same date as the one issued by the Agent to the buyer (Customer). The invoice number is assigned in accordance with the individual chronology of the Principal's invoices. In the line "Seller" the details of the Principal are indicated. The line “Buyer” indicates the name of the actual buyer (Customer), and not the Agent (clauses “and” clause 1 of the Rules for filling out an invoice of Resolution No. 1137, letter of the Ministry of Finance of Russia dated May 10, 2012 No. 03-07-09/47) . The tabular part repeats all the data of the invoice issued by the Agent to the buyer (Customer). The Agent registers the document received from the Principal in Part 2 of the log of received and issued invoices used in calculations of value added tax, Resolution No. 1137.

At the same time, the Agent issues invoices to the Principal for the amounts of his agency fee for services provided under the agency agreement and registers them in the sales book (clause 20 of the Rules for maintaining the sales book used in calculations of value added tax, Resolution No. 1137 ).

If the Agent receives funds from the Principal in the form of payment (partial payment) for the upcoming provision of intermediary services (prepayment of remuneration), the Agent must issue an invoice to the Principal for the received payment amount (partial payment) and register it in his sales book.

The Principal registers the invoice received from the Agent for the amount of the agent's remuneration in Part 2 of the journal for recording received and issued invoices used in calculations of value added tax, Resolution N 1137 and in the purchase book (clause 11 of the Rules for maintaining the purchase book used when calculating value added tax, Resolution No. 1137).

Let us note once again that invoices issued by the Agent to Buyers (Customers) on its own behalf during the implementation of work (services), as well as issued to Buyers (Customers) upon receipt of payment amounts (partial payment) from them for the upcoming provision of services (performance of work) ), are not registered in the Agent's sales book (clause 20 of the Rules for maintaining the sales book used in calculations of value added tax, Resolution No. 1137).

Agent Accounting

The income of the organization, depending on its nature, the conditions for receiving it and the areas of the organization’s activities, are divided into income from ordinary activities and other income (clause 4 of PBU 9/99 “Income of the organization” (hereinafter referred to as PBU 9/99)). Income other than income from ordinary activities is considered other income. In this case, the organization independently recognizes receipts as income from ordinary activities or other income based on the requirements of PBU 9/99, the nature of its activities, the type of income and the conditions for their receipt.

Depending on the qualification of income in the form of agency fees, it can be reflected either in the “Sales” account, intended for accounting for income from ordinary activities, or in the “Other income and expenses” account (Instructions for using the Chart of Accounts for accounting financial and economic activities of organizations , approved by order of the Ministry of Finance of Russia dated October 31, 2000 N 94n (hereinafter referred to as the Instructions)).

It should be noted that receipts from other legal entities and individuals, including under agency agreements in favor of the Principal, are not recognized as income of the organization (clause 3 of PBU 9/99). Consequently, funds received by the Agent from the Customers, subject to transfer to the Principal, are not included in the Agent’s income and are recorded in the settlement accounts.

In accordance with the Instructions, settlements with the principal can be recorded in the account "Settlements with various debtors and creditors", the subaccount "Settlements with the principal".

Transactions related to the execution of an agency agreement can be reflected in the Agent’s accounting accounts as follows:

Debit () Credit, subaccount "Calculations for advances received"

- received an advance from the customer;

Debit Credit, subaccount "Settlements with the principal"

- the sale of services (work) under the agency agreement is reflected;

Debit, subaccount "Settlements on advances received" Credit

- the advance amount has been credited;

Debit () Credit

- funds were received from the customer in the manner of final payment;

- funds, minus the retained agency fee, are transferred to the principal;

Debit Credit, subaccount "Revenue" (91, subaccount "Other income")

- revenue is reflected in the form of agency fees;

Debit, subaccount "Settlements with the principal" Credit

- offset of agency fees is reflected;

Debit 90-3 Credit 68-2

- VAT is charged on agency fees.

The amount of agency fees is recognized as the Agent’s income, subject to income tax. At the same time, when determining the tax base for the Agent’s income tax, income in the form of property (including cash) received by the Agent in connection with the fulfillment of obligations under the agency agreement, as well as for reimbursement of expenses incurred by the Agent for the Principal, is not taken into account, if such expenses are not are subject to inclusion in the agent’s expenses in accordance with the terms of concluded contracts (clause 9, clause 1, article 251 of the Tax Code of the Russian Federation). That is, the Agent’s income taken into account for tax purposes includes the amount of agency remuneration (money received from Customers and subject to transfer to the Principal is not the Agent’s income).

Income for profit tax purposes is recognized in the reporting (tax) period in which it occurred, regardless of the actual receipt of funds, other property (work, services) and (or) property rights (accrual method) (clause 1 of Art. 271 of the Tax Code of the Russian Federation). In this case, regardless of the moment of actual receipt of the amounts of agency remuneration from the Principal to the Agent’s account (in this case, regardless of the date of deduction by the Agent of the remuneration from the amounts due to the Principal), the date of recognition of income for profit tax purposes for the Agent will be the date of submission of the report by the Agent (within the time limits specified agreement) or the date of signing by the parties (Agent and Principal) of the act of provision of services (depending on what form of the Agent’s report to the Principal is stipulated by the terms of the agency agreement) (clause 3 of Article 271 of the Tax Code of the Russian Federation).

The Agent's obligation to pay VAT to the budget (if the Agent applies the general taxation system and is a VAT payer) arises only from the amount of the agency fee (clause 1 of Article 156 of the Tax Code of the Russian Federation).

Accounting with the Principal

Reflection in the accounting and tax accounting of the Principal of transactions performed under the agency agreement must be carried out on the basis of the Agent’s report, to which supporting documents are attached (Article 1008 of the Civil Code of the Russian Federation).

Transactions related to the execution of an agency agreement can be reflected in the Principal’s accounting accounts as follows:

Debit Credit, subaccount "Settlements with agent"

- the amount transferred by the agent under the agency agreement from buyers of services (customers) is taken into account, minus the agent’s remuneration;

Debit, subaccount "Settlements with agent" Credit

- the agent's remuneration is included in the payment from buyers.

The Principal’s income, taken into account when forming taxable profit, will be the entire amount of proceeds from the sale of work (services), that is, the amount for which the work was sold to the Customers by the Agent, minus VAT (clause 1 of Article 248, clause 1 of Article 249 of the Tax Code of the Russian Federation ). At the same time, the Principal will be able to take into account the amount of the agent’s remuneration (clause 3, clause 1, article 264 of the Tax Code of the Russian Federation), as well as the cost of the work (services) performed, as part of expenses, provided that the costs incurred meet the criteria provided for in clause 1 of Art. 252 of the Tax Code of the Russian Federation.

For a Principal using the accrual method, the amount of money received as an advance payment for the upcoming performance of work (provision of services) is not taken into account for income tax purposes (clause 1, clause 1, article 251 of the Tax Code of the Russian Federation).

The tax base for VAT for the Principal is the total amount of services provided (work performed), since the Principal is their performer (clause 1, clause 1, article 146 of the Tax Code of the Russian Federation, clause 1, article 167, clause 1, article 154 of the Tax Code of the Russian Federation ). It is necessary to take into account, since in accordance with paragraph 1 of Art. 167 of the Tax Code of the Russian Federation, the tax base for calculating VAT is the earliest of the dates (the day of shipment of work (services) or the day of payment (partial payment)), then if the Agent receives an advance payment from the Customer, the Principal will have to charge VAT on the amount of the advance payment, since he owns everything received by the intermediary in the transaction. In order for the Principal to be able to charge VAT on the advance payment, the Agent must inform him of the advance received.

Encyclopedia of solutions. Agent reports;

Encyclopedia of solutions. Execution of the agency agreement;

Encyclopedia of solutions. Accounting with the principal when selling goods through a commission agent;

Encyclopedia of solutions. Accounting with the commission agent when selling the principal's goods.

Prepared answer:

Expert of the Legal Consulting Service GARANT

Member of the Chamber of Tax Advisors Alekseeva Anna

Response quality control:

Reviewer of the Legal Consulting Service GARANT

auditor, member of the MoAP Melnikova Elena

The material was prepared on the basis of individual written consultation provided as part of the Legal Consulting service.